Dear Bankers

ALL INDIA BANK EMPLOYEES' ASSOCIATION

Central Office: “PRABHAT NIVAS” Regn. No.2037

Singapore Plaza, 164, Linghi Chetty Street, Chennai-600001...

Phone: 2535 1522, 6543 1566 Fax: 4500 2191, 2535 8853

e mail ~ chv.aibea@gmail.com & aibeahq@gmail.com

FOR THE INFORMATION OF OUR UNITS AND MEMBERS:

Today, the distribution chart has been signed between IBA and our Unions covering the allocation to various heads. Payscales and Allowances are as under:

. Pay Scales: from 1-11-2012

Clerk: 11765 – 655/3 –815/3 –980/3 –1145/7 –2120 –1310/1– 31540 – 1310 x 8 = 42,020

Substaff : 9560 – 325/4 – 410 /5 – 490/4 – 570/3 – 655/3 – 18545 – 655 x 8 = 23785

Stagnation increments: 8 : Substaff: 8 x 2 years ; Clerk : 5 x 3 years + 3 x 2 years

. Dearness Allowance: 0.10 % per slab of 4 points over 4440 points

. HRA : 45 lacs and above: 10 % ; 12-45 lacs & Goa : 9 % ; other centres : 7.5 %

. Transport Allowance: upto 15th Stage : Rs. 425 and others : Rs. 470

. Special Pay:

i) SWO-B: 820; Head cashier: 1280; Spl. Asst. 1930

ii) Armed Guard/Bill Collector: 390; Daftary: 560; Head Peon: 740; Driver: 2370; Electrician/AC Plant Helper: 2040, Head messenger in IOB: 1630

. PQP : Rs. 410, 800, 1210 , 1620, 2010

. FPP : Clerk: Rs. 1310 / 1580, 1570, 1550, 1550 / 1450

Substaff: Rs. 655 / 790, 890, 780, 780 / 730

. Medical Aid : Rs. 2200 per year

. Special Allowance ( new allowance ) :

7.75 % of Basic pay; DA is payable on this allowance

The full Settlement is under preparation and is expected to be signed on the 25th May, 2015 (Monday).

Flash: Yesterday, RBI has given its in principle ok for implementing Full holidays on 2nd and 4th Saturday. Matter is being expedited with the Government now

Signing of 10th BPS by 23rd May 2015 May Not Happen In view of Acceptance of Writ of WE BANKERS and Ignoring the Issues of Retired Bankers by IBA and UFBU-By Rajesh Goyal -20.05.2015

By now all bankers are aware that the 90 days period sought by UFBU and IBA is coming to an end in next 5 days. As the BPS has already become overdue by over 30 months, and pressure in social media has tremendously increased, UFBU is in a great hurry to sign the BPS. However, they are not disclosing the details to anybody and in view of lack of trust towards IBA and UFBU, they fear this BPS will be the worst.

RBI gives banks provisioning leeway for reporting frauds on time-DNA

Rising number of frauds especially on high value corporate loans has forced the Reserve Bank of India (RBI) to dangle a carrot to banks in order to report diversion of funds on time.

If banks report frauds on time, they can stagger the provisioning in four quarters, providing 25% each quarter. When the account is declared as fraud, banks have to immediately set aside money as buffer equivalent to the loans extended to the borrower. But if not reported on time, then banks will have to provision 100% at one shot.

For instance, if a bank has lent Rs 100 crore to a borrower who is declared fraud, then the bank has to set aside Rs 100 crore as provision immediately, and if it is reported on time, they can stagger the repayment over four quarters, that is in this case Rs 25 crore a quarter.

A senior RBI official said, "We are incentivising banks to report frauds so that they will be encouraged to report fraudulent cases faster rather than brushing it under the carpet. We were forced to declare REI Agro a fraud case as some banks were classifying it as non-performing asset (NPA) standard while some banks declared as an NPA account."

Some of the bank loans to REI Agro (Rs 4,000 crore), Winsome Diamonds (Rs 3,500 crore), Electrotherm India Ltd (Rs 434 crore) have already been listed as frauds.

The central bank has meanwhile asked banks to undertake a forensic audit on Winsome Diamonds. Last year, the company was referred to the special corporate debt restructuring cell but failed to get special package from banks as some of the banks were not convinced with the submission of the management that receivables from customers for the diamonds exported failed to come through, resulting in the company defaulting on payments.

A senior banker with a public sector bank said, "The problem for bankers is that once the case gets handed over to the investigating agency, the needle of suspicion begins from the bank. They will first come up with a conspiracy theory saying that they may have been a connivance with the bank officials. So bankers desist from reporting the frauds. Often bankers are caught and the promoters would be absconding."

The Kolkata-based REI Agro, which specialised in Basmati rice exports, was declared fraud by the central bank after some banks classified it as a fraud. Bankers allege that the company may have diverted the money overseas.

Just last year, 20 banks lent REI working capital finance of Rs 4,000 crore under the Joint Lenders Forum (JLF) to work out a corrective action plan for the financially-stressed company. The company defaulted on its payment to certain lenders, which even led to a winding-up petition filed by the United Bank of India in the Calcutta High Court.

A senior RBI official confirmed that the account has been declared a fraud for alleged diversion of funds, and the Central Bureau of Investigation (CBI) is investigating after some banks handed over the case to CBI. This is the only bank loan that has been declared as a fraud by RBI and have asked all lenders to classify it as a non-performing asset even if the promoters are repaying the money.

Central Bank of India handed over its exposure to the Ahmedabad-based Electrotherm for an alleged fraud. CBI came out with a report in August last year that it had registered a case against the directors of Electrotherm for entering into a criminal conspiracy and cheating the bank to the tune of Rs 438 crore.

Is RBI downplaying the bad-loans problem?

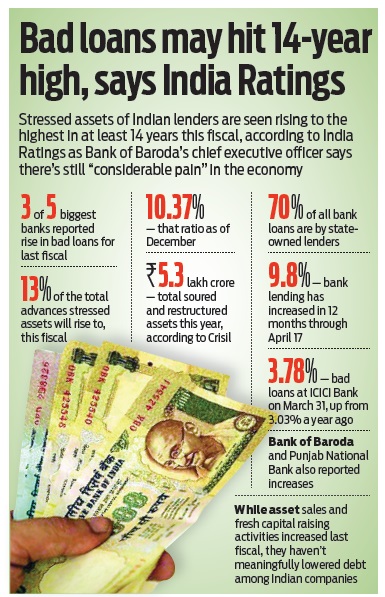

Bad loans of Indian banks are seen rising to their highest levels in nearly 14 years, India Ratings has warned.

The ratings agency further said that it estimates total impaired loans at 13% (of overall loan book) for FY16. 4.9% of this would be gross non-performing loans and the rest would be restructured loans, etc.

Three out of the five big banks in India have reported a hike in non-performing assets for last fiscal. Crisil, too, has highlighted the bad loans problem and pointed out that the total amount of assets gone bad and restructured to hit Rs 5.3 lakh crore this year. NPAs are likely to be at Rs 4 lakh crore, up by Rs 60,000 crore from last year.

In January this year, shares of ICICI Bank and Bank of Baroda plunged as their bad-loans provisions saw a jump.

Bank of Baroda's provisions grew by 66% for the last quarter of the year and ICICI Bank increased its cushioning by 41%.

As recent as in April this year, shares of ICICI Bank tumbled further as the bank posted low profit as its gross non-performing assets grew to 3.78% from 3.03% as against the same period a year before.

Moreoever, India Spend, in February reported that bad-loans rose by 20% from April to December 2014 in public sector banks that account for over 70% of India's commercial lending.

Gross NPAs, it reported, rose to Rs 2.73 lakh crore and if combined with restructured assets, the number stood at nearly Rs 5.5 lakh crore.

RBI data shows that as on March 31, 2015, gross NPAs stood at 4.45%. That is, for every Rs 100 given as a loan, Rs 4.45 is lost in bad assets.

However, none of this is shaking Reserve Bank of India's (RBI) chief Raghuram Rajan's belief. He maintained that these bad assets won't lead to a financial crisis. He acknowledged that improvements in credit quality is going to be slow but ruled out the issue ballooning into a crisis.

The RBI governor, on May 15, categorically denied that India isn't in danger of a financial crisis.

NPAs, as India Ratings, suggest, are on the rise and may hit a 14-year peak if corrective action isn't taken.

With the slow economic recovery, this seems a tall order.

PTI has reported, "The stressed assets ratio, which includes NPAs and restructured loans, of public sector banks has risen by an alarming 131 bps to 13.2% or over Rs 7,12,000 crore, in FY15 with their gross non-performing assets touching 5.17%. This is nearly 230 bps more than that of the system, according to the RBI data."

http://www.dnaindia.com/money/report-rbi-gives-banks-provisioning-leeway-for-reporting-frauds-on-time-2087009

The tussle between Delhi government and its bureaucracy could jeopardise the Rs 11,000-crore loan approved by a group of lenders led by state-owned Power Finance Corporation (PFC) to Reliance Infrastructure’s power distribution companies (discoms) — BSES Yamuna and BSES Rajdhani — in the capital.

The final disbursal of loan is subject to a letter of comfort (LoC) to be issued by the Delhi government to the lenders as it holds 49% stake in the discoms and a third one run by a Tata Power subsidiary in the national capital region.

Delhi chief minister Arvind Kejriwal had opposed the appointment of Shakuntala Gamlin, principal secretary for power, as acting chief secretary of the state, alleging that she was lobbying for LoC on behalf of the discoms. “The two companies are joint ventures, where the Delhi government has a 49% shareholding. BSES companies are managed by board of directors, where 4 out of 9 members are nominated by the government and are senior IAS officers,” BSES wrote to Najeeb Jung, lieutenant governor of Delhi, clarifying its position in the aftermath of controversy concerning the LoC. It added that the LoC has been sought by PFC and not by Reliance Infra.

In another letter reviewed by FE, BSES has written to the principal secretary of finance on March 30 with details of the loan and had asked issuance of a ‘strong’ comfort letter to PFC.

“…PFC sanction alongwith the scheme of proposal, terms and conditions and proposed utilisation was duly considered and approved by the board of directors (including GoNCTD nominees) of BRPL and BYPL in a meeting on March 26, 2015,” it wrote.

The advances will enable the two discoms, under stress due to delays in monetisation of regulatory assets, to retire existing debt of half the size from a 19-bank consortium led by State Bank of India and pay the dues to the generation and transmission companies. The new loan will come with an interest relief of 1.5-2% that could bring down the cost of power by 13 paise per unit.

The Delhi government has been no stranger to issuing LoCs on behalf of the power companies in the past. It had issued LoC to NTPC in December 2011 to ensure that power supply remained uninterrupted. In May 2014, an LoC was granted to PFC and REC for raising short-term loans of R1,000 crore to pay power supplier dues in compliance of orders of the Supreme Court.

Of the R11,000-crore loan, about R5,000 crore will be disbursed by PFC while the rest will be available from other lenders in the consortium, a PFC source told FE. The tenure of the new loan, if approved, could be for a period of seven to eight years and the interest savings for the BSES firms would translate to about R250 crore annually.

RInfra will be pledging its entire 51% of shareholding in BSES discoms to the PFC-led consortium to avail the loan.

The discoms have been urging the state government since early January for a LoC for the loan approval. The Arvind Kejriwal-led government, which has ordered a CAG audit of the three Delhi discoms (Tata Power Delhi Distribution and the two BSES discoms), is yet to give any commitment on this.

ALL INDIA BANK EMPLOYEES' ASSOCIATION

Central Office: “PRABHAT NIVAS” Regn. No.2037

Singapore Plaza, 164, Linghi Chetty Street, Chennai-600001...

Phone: 2535 1522, 6543 1566 Fax: 4500 2191, 2535 8853

e mail ~ chv.aibea@gmail.com & aibeahq@gmail.com

FOR THE INFORMATION OF OUR UNITS AND MEMBERS:

Today, the distribution chart has been signed between IBA and our Unions covering the allocation to various heads. Payscales and Allowances are as under:

. Pay Scales: from 1-11-2012

Clerk: 11765 – 655/3 –815/3 –980/3 –1145/7 –2120 –1310/1– 31540 – 1310 x 8 = 42,020

Substaff : 9560 – 325/4 – 410 /5 – 490/4 – 570/3 – 655/3 – 18545 – 655 x 8 = 23785

Stagnation increments: 8 : Substaff: 8 x 2 years ; Clerk : 5 x 3 years + 3 x 2 years

. Dearness Allowance: 0.10 % per slab of 4 points over 4440 points

. HRA : 45 lacs and above: 10 % ; 12-45 lacs & Goa : 9 % ; other centres : 7.5 %

. Transport Allowance: upto 15th Stage : Rs. 425 and others : Rs. 470

. Special Pay:

i) SWO-B: 820; Head cashier: 1280; Spl. Asst. 1930

ii) Armed Guard/Bill Collector: 390; Daftary: 560; Head Peon: 740; Driver: 2370; Electrician/AC Plant Helper: 2040, Head messenger in IOB: 1630

. PQP : Rs. 410, 800, 1210 , 1620, 2010

. FPP : Clerk: Rs. 1310 / 1580, 1570, 1550, 1550 / 1450

Substaff: Rs. 655 / 790, 890, 780, 780 / 730

. Medical Aid : Rs. 2200 per year

. Special Allowance ( new allowance ) :

7.75 % of Basic pay; DA is payable on this allowance

The full Settlement is under preparation and is expected to be signed on the 25th May, 2015 (Monday).

Flash: Yesterday, RBI has given its in principle ok for implementing Full holidays on 2nd and 4th Saturday. Matter is being expedited with the Government now

Signing of 10th BPS by 23rd May 2015 May Not Happen In view of Acceptance of Writ of WE BANKERS and Ignoring the Issues of Retired Bankers by IBA and UFBU-By Rajesh Goyal -20.05.2015

By now all bankers are aware that the 90 days period sought by UFBU and IBA is coming to an end in next 5 days. As the BPS has already become overdue by over 30 months, and pressure in social media has tremendously increased, UFBU is in a great hurry to sign the BPS. However, they are not disclosing the details to anybody and in view of lack of trust towards IBA and UFBU, they fear this BPS will be the worst.

The time of writing this article is 19th May 2015 (Night), Since morning, we have been receiving different messages which are contradictory in nature.

In morning one of the message received from some authentic source read as “Wage revision talks with IBA progressing steadily and we expect to conclude entire process and sign anytime between 21st and 23rd May”.

Then I came across a news from Kanpur, wherein it is reported that WE BANKERS have been able to get an order from High Court. This news has also been published in local newspapers, cutting of which is pasted below. Although final orders have not been seen by me but it appears HC has asked the CLC to settle the dispute raised by WE BANKERS within six months. This order is yet to be placed before CLC. WE BANKERS are hopeful that now IBA and UFBU will not be able to sign the 10th BPS till they are also heard by CLC.

At the same time, UFBU and IBA has antagonized the retired bankers as they have reported to have excluded the demands of retired bankers from talks and they are not likely to form part of the 10th BPS. This Group too is looking for ways to stop the signing of 10th BPS till their demands are also considered and form part of the 10th BPS as has been the tradition in past BPS.

Thus, a group of bankers seems to be of the strong view that IBA and UFBU will not be able to sign the settlement immediately as one of the groups will bring stay order.

All the above has raised confusion as to whether the 10th BPS will be really signed by 23rd May, 2015. Even if signed, will they be able to implement the same before a Court stays the same?

However, UFBU has started a campaign, in the hope to sign the BPS latest by 25th May 2015, to release various types of charts through their local units which give you a broad overview of the things that are likely to be signed. However, nothing is confirmed and all that is being circulated is tentative and is subject to change even at the last moment.

Based on the past trends, I personally feel it will be quite difficult for WE BANKERS and Retired Banker associations to stop the signing of 10th BPS as IBA with money and muscle power is likely to push this through as it suits them. By showing the threat of Court stay IBA is likely to create a fear among UFBU who will now be ready to sign on the dotted lines as they do not have time to think and discuss it further. Thus, the end result will be that 10th BPS may be signed as per wishes of IBA and may be kept in abeyance for few days, if any of the above two organizations are able to bring the Court stay.

After studying some of the Charts in circulation, it seems now IBA has sticked to its stand of 2% increase in Basic Pay but agreed to introduce Grade Pay / Special Pay, instead of loading the remaining 13% in HRA and transport only. The circulars now going around show that even DA will be payable on these Special / Grade pay. It seems because of the hue and cry generated by the exposure of ABS in its articles about merely 2% increase in BP, UFBU and IBA came on backfoot and thus agreed to introduce Grade Pay / Spl Pay. It is a good sign. But the question arises, why IBA was still interested to keep Basic Pay low and allow separate Grade Pay with DA? There must be some hidden agenda which we can comment only when final agreement is signed and put in public domain.

I have a gut feeling that there will be some surprise element, which can be extremely detrimental to a group of the bankers. Will the Grade Pay and DA on this will form part of “Pay” for the purpose of calculation of superannuation benefits like Pension, Gratuity, commutation etc. If UFBU agrees that any of these will not be accounted towards superannuation benefits then the bankers who are retiring by 2017 will suffer the maximum. We know there is maximum retirement by 2017. If this is the agreement, then it will amount to cheating with the senior bankers and it will bring lot of resentment, which will then be reflected in the growth of the banking till 2019 or so.

Thus, as on late night of 19th May or early 20th May, 2015, things are still in fluid state and we have to wait for another 48 hours till we hear something concrete on this issue.

RBI gives banks provisioning leeway for reporting frauds on time-DNA

Rising number of frauds especially on high value corporate loans has forced the Reserve Bank of India (RBI) to dangle a carrot to banks in order to report diversion of funds on time.

If banks report frauds on time, they can stagger the provisioning in four quarters, providing 25% each quarter. When the account is declared as fraud, banks have to immediately set aside money as buffer equivalent to the loans extended to the borrower. But if not reported on time, then banks will have to provision 100% at one shot.

For instance, if a bank has lent Rs 100 crore to a borrower who is declared fraud, then the bank has to set aside Rs 100 crore as provision immediately, and if it is reported on time, they can stagger the repayment over four quarters, that is in this case Rs 25 crore a quarter.

A senior RBI official said, "We are incentivising banks to report frauds so that they will be encouraged to report fraudulent cases faster rather than brushing it under the carpet. We were forced to declare REI Agro a fraud case as some banks were classifying it as non-performing asset (NPA) standard while some banks declared as an NPA account."

Some of the bank loans to REI Agro (Rs 4,000 crore), Winsome Diamonds (Rs 3,500 crore), Electrotherm India Ltd (Rs 434 crore) have already been listed as frauds.

The central bank has meanwhile asked banks to undertake a forensic audit on Winsome Diamonds. Last year, the company was referred to the special corporate debt restructuring cell but failed to get special package from banks as some of the banks were not convinced with the submission of the management that receivables from customers for the diamonds exported failed to come through, resulting in the company defaulting on payments.

A senior banker with a public sector bank said, "The problem for bankers is that once the case gets handed over to the investigating agency, the needle of suspicion begins from the bank. They will first come up with a conspiracy theory saying that they may have been a connivance with the bank officials. So bankers desist from reporting the frauds. Often bankers are caught and the promoters would be absconding."

The Kolkata-based REI Agro, which specialised in Basmati rice exports, was declared fraud by the central bank after some banks classified it as a fraud. Bankers allege that the company may have diverted the money overseas.

Just last year, 20 banks lent REI working capital finance of Rs 4,000 crore under the Joint Lenders Forum (JLF) to work out a corrective action plan for the financially-stressed company. The company defaulted on its payment to certain lenders, which even led to a winding-up petition filed by the United Bank of India in the Calcutta High Court.

A senior RBI official confirmed that the account has been declared a fraud for alleged diversion of funds, and the Central Bureau of Investigation (CBI) is investigating after some banks handed over the case to CBI. This is the only bank loan that has been declared as a fraud by RBI and have asked all lenders to classify it as a non-performing asset even if the promoters are repaying the money.

Central Bank of India handed over its exposure to the Ahmedabad-based Electrotherm for an alleged fraud. CBI came out with a report in August last year that it had registered a case against the directors of Electrotherm for entering into a criminal conspiracy and cheating the bank to the tune of Rs 438 crore.

Is RBI downplaying the bad-loans problem?

Bad loans of Indian banks are seen rising to their highest levels in nearly 14 years, India Ratings has warned.

The ratings agency further said that it estimates total impaired loans at 13% (of overall loan book) for FY16. 4.9% of this would be gross non-performing loans and the rest would be restructured loans, etc.

Three out of the five big banks in India have reported a hike in non-performing assets for last fiscal. Crisil, too, has highlighted the bad loans problem and pointed out that the total amount of assets gone bad and restructured to hit Rs 5.3 lakh crore this year. NPAs are likely to be at Rs 4 lakh crore, up by Rs 60,000 crore from last year.

In January this year, shares of ICICI Bank and Bank of Baroda plunged as their bad-loans provisions saw a jump.

Bank of Baroda's provisions grew by 66% for the last quarter of the year and ICICI Bank increased its cushioning by 41%.

As recent as in April this year, shares of ICICI Bank tumbled further as the bank posted low profit as its gross non-performing assets grew to 3.78% from 3.03% as against the same period a year before.

Moreoever, India Spend, in February reported that bad-loans rose by 20% from April to December 2014 in public sector banks that account for over 70% of India's commercial lending.

Gross NPAs, it reported, rose to Rs 2.73 lakh crore and if combined with restructured assets, the number stood at nearly Rs 5.5 lakh crore.

RBI data shows that as on March 31, 2015, gross NPAs stood at 4.45%. That is, for every Rs 100 given as a loan, Rs 4.45 is lost in bad assets.

However, none of this is shaking Reserve Bank of India's (RBI) chief Raghuram Rajan's belief. He maintained that these bad assets won't lead to a financial crisis. He acknowledged that improvements in credit quality is going to be slow but ruled out the issue ballooning into a crisis.

The RBI governor, on May 15, categorically denied that India isn't in danger of a financial crisis.

NPAs, as India Ratings, suggest, are on the rise and may hit a 14-year peak if corrective action isn't taken.

With the slow economic recovery, this seems a tall order.

PTI has reported, "The stressed assets ratio, which includes NPAs and restructured loans, of public sector banks has risen by an alarming 131 bps to 13.2% or over Rs 7,12,000 crore, in FY15 with their gross non-performing assets touching 5.17%. This is nearly 230 bps more than that of the system, according to the RBI data."

http://www.dnaindia.com/money/report-rbi-gives-banks-provisioning-leeway-for-reporting-frauds-on-time-2087009

Rs 11k-cr loan to Reliance Infra discoms could be in jeopardy-Financial Express

Tussle between Delhi govt and bureaucracy stands in the way of loan disbursal to Reliance Infra discoms

Delhi chief minister Arvind Kejriwal had opposed the appointment of Shakuntala Gamlin, principal secretary for power, as acting chief secretary of the state, alleging that she was lobbying for LoC on behalf of the discoms.

The final disbursal of loan is subject to a letter of comfort (LoC) to be issued by the Delhi government to the lenders as it holds 49% stake in the discoms and a third one run by a Tata Power subsidiary in the national capital region.

Delhi chief minister Arvind Kejriwal had opposed the appointment of Shakuntala Gamlin, principal secretary for power, as acting chief secretary of the state, alleging that she was lobbying for LoC on behalf of the discoms. “The two companies are joint ventures, where the Delhi government has a 49% shareholding. BSES companies are managed by board of directors, where 4 out of 9 members are nominated by the government and are senior IAS officers,” BSES wrote to Najeeb Jung, lieutenant governor of Delhi, clarifying its position in the aftermath of controversy concerning the LoC. It added that the LoC has been sought by PFC and not by Reliance Infra.

In another letter reviewed by FE, BSES has written to the principal secretary of finance on March 30 with details of the loan and had asked issuance of a ‘strong’ comfort letter to PFC.

“…PFC sanction alongwith the scheme of proposal, terms and conditions and proposed utilisation was duly considered and approved by the board of directors (including GoNCTD nominees) of BRPL and BYPL in a meeting on March 26, 2015,” it wrote.

The advances will enable the two discoms, under stress due to delays in monetisation of regulatory assets, to retire existing debt of half the size from a 19-bank consortium led by State Bank of India and pay the dues to the generation and transmission companies. The new loan will come with an interest relief of 1.5-2% that could bring down the cost of power by 13 paise per unit.

The Delhi government has been no stranger to issuing LoCs on behalf of the power companies in the past. It had issued LoC to NTPC in December 2011 to ensure that power supply remained uninterrupted. In May 2014, an LoC was granted to PFC and REC for raising short-term loans of R1,000 crore to pay power supplier dues in compliance of orders of the Supreme Court.

Of the R11,000-crore loan, about R5,000 crore will be disbursed by PFC while the rest will be available from other lenders in the consortium, a PFC source told FE. The tenure of the new loan, if approved, could be for a period of seven to eight years and the interest savings for the BSES firms would translate to about R250 crore annually.

RInfra will be pledging its entire 51% of shareholding in BSES discoms to the PFC-led consortium to avail the loan.

The discoms have been urging the state government since early January for a LoC for the loan approval. The Arvind Kejriwal-led government, which has ordered a CAG audit of the three Delhi discoms (Tata Power Delhi Distribution and the two BSES discoms), is yet to give any commitment on this.

No comments:

Post a Comment