Banks write off Rs 2.2 lakh crore in five years, said to be highest ever

BY SATYANARAYAN IYER, TNN | MAY 27, 2017, PUNE:

All scheduled commercial banks (SCBs) wrote off Rs 2,25,180 crore cumulatively in the five year period ended March 2016, the Reserve Bank of India (RBI) said in an RTI reply filed by TOI.

SCBs represent all public sector banks, private sector banks, foreign banks, regional rural banks and some cooperative banks. These represent over 95% of the formal credit given out by all financial institutions in the country.

"This could be the highest ever write off in a five year period in absolute terms as are the total stressed assets in the banking system," said Abhishek Bhattacharya, director and co-head for financial institution India Ratings.

Banks and the RBI have often stated that these write offs are just technical in nature and an exercise to clean up the balance sheets. They have further argued that banks continue to retain the right to recovery from these written off accounts.

"Writing off of nonperforming assets (NPAs) is a regular exercise conducted by banks to clean up their balance sheets. A substantial portion of this write off is, however, technical in nature. It is primarily aimed at cleansing the balance sheet and achieving taxation efficiency. In 'technically written off' accounts, loans are written off from the books at the head office, without foregoing the right to recovery. Further, write offs are 'generally' carried out against accumulated provisions made for such loans. Once recovered, the provisions made for those loans flow back into the profit and loss account of banks," the RBI said in a clarification to a media report, based on an RTI reply in February 2016.

Be that as it may, the recovery from written off accounts constitute only a tiny fraction of the overall written off accounts, available data shows. In the financial year 201415, banks could recover only 11.85% (Rs 6,968 crore) of the written off accounts in that year and 13.8% (Rs 9,717 crore) of the written off accounts in FY 201516. The data for previous three years is not available with the RBI, it said.

"The information on recovery from written off accounts from FY 201112 to 201314 is not available with us," the RBI said in its RTI reply. Though the amount from recovered loans in FY15 and FY16 might not pertain to that financial year alone, the numbers show the actual recovery to be only a tiny fraction of the total amount written off and also to be a long protracted process.

In each of these five years, loans written off showed an increasing trend — at an average addition of over Rs 12,000 crore each year. The worst year was FY15, when banks cumulatively wrote off Rs 16,550 crore more than the previous year. Banks reduce written off loan accounts from their overall nonperforming assets.

Adding the same back, the actual gross NPAs at banks could look a lot worse every subsequent year than it already does. Written off loans accounted for 1116% of overall bad loans of the bank in each of those years (see table). Since 2011, banks started lending heavily to large corporates and, according to analysts, the problem suddenly became a lot bigger as "corporate leveraged built up".

The traditional tools of recovery like debt recovery tribunals, and Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (Sarfaesi) Act, 2002, have become blunt in the face of such huge bad loans from large corporate accounts.

"Newer mechanisms are needed to deal with these big loans and they have to be dealt with on a goingconcern basis. The usual recovery mechanism will not work," according to Bhattacharya. He added, "Recovery will take time and won't happen in a hurry."

The RBI said in its RTI reply that it did not have the required data on the "number" of loans written off by banks and the "sectoral breakup of reduction in NPAs due to writeoffs," by SCBs for the years FY12 16. However, most analysts believe that the bulk of the writeoffs were primarily in the large corporate accounts. Also, though the percentage of writtenoff accounts as a share of NPAs is lower in FY 201516, it is primarily because the NPAs grew a massive Rs 2,56, 848 crore in the year.

Government to step up mergers in PSU banks: Arun Jaitley

TNN | Updated: May 28, 2017,

HIGHLIGHTS

The government has expressed its intention of consolidation in the public sector banking space against the backdrop of the mountain of bad loans.

Finance minister Arun Jaitley said that govt's aim is to have a handful of strong and bigger banks of international level.

NEW DELHI: The Centre will pursue more mergers in the state-run banking space as the aim is to have a handful of strong and bigger banks of international level, finance minister Arun Jaitley has said. "Today banking is not what it used to be 10-20 years ago... Is it necessary to have 30-32 public sector banks, some of them weak? Obviously not. What will you do with weak banks," he said on DD News.

"We have merged five subsidiaries of SBI and the Bharatiya Mahila Bank with SBI. I have announced that we want fewer banks but bigger and stronger banks which can be of international level. In the coming days most probably we will move faster in this direction," Jaitley said. The government has expressed its intention of consolidation in the public sector banking space against the backdrop of the mountain of bad loans.

The Bharatiya Mahila Bank and five associates lender merged with the State Bank of India (SBI) on April 1, pushing the country's largest lender among the top 50 banks globally.

State Bank of Bikaner and Jaipur (SBBJ), State Bank of Hyderabad (SBH), State Bank of Mysore (SBM), State Bank of Patiala (SBP) and State Bank of Travancore (SBT), besides Bharatiya Mahila Bank (BMB), merged with SBI.

The total customer base of the bank will reach 37 crore with a branch network of around 24,000 and nearly 59,000 ATMs across the country. The new entity will have deposits of over Rs 26 lakh crore and advances level of Rs 18.50 lakh crore.

ICICI Bank hikes CEO Chanda Kochhar's salary by 64% ; She now earns Rs 2.1 lakh a day

In FY17, Kocchar's remuneration included a bonus of Rs 2.2 crore, according to ICICI Bank's annual report.

Beena Parmar, Moneycontrol News

A performance bonus of Rs 2.20 crore spikes ICICI Bank chief Chanda Kochhar’s total remuneration by 63.8 percent for the fiscal year ending March 2017 at Rs 7.85 crore. In other words, Kochhar now draws Rs 65 lakh a month, or Rs 2.1 lakh per day.

Apart from the basic salary, the remuneration includes allowances and perquisites and contribution to provident, superannuation and gratuity funds. This, however, excludes employee stock options which stood at Rs 13.75 lakh subject to Reserve Bank of India (RBI) approval.

In FY16, Kochhar was the third-highest paid banking chief after HDFC Bank's head Aditya Puri and Axis Bank's captain Shikha Sharma. Puri earned a remuneration of Rs 9.7 crore for FY16 while Sharma earned Rs 5.5 crore during the year. Kochhar's pay was significantly lower at Rs 4.79 crore in FY16, according to the bank's annual report.

Without the bonus and other variables, Kochhar’s basic salary increased by 15 percent to Rs 2.67 crore in FY17 as against Rs 2.32 crore for FY16.

The hike in the total remuneration in FY17 was primarily driven by the performance bonus which the ICICI Bank CEO and the entire senior management had forgone a year ago owing to the bank’s weak financial results.

ICICI Bank had posted ones of its worst quarterly performance in the decade with a net profit drop of 87 percent for the March quarter in FY16. After forgoing the bonus in FY16, the senior management got a total performance bonus of Rs 7.55 crore in FY17.

The percentage increase in the median remuneration of all employees in the FY17 was around 12 percent.

The annual report highlighted that the average percentage increase made in the salaries of total employees other than the Key Managerial Personnel (senior management) for fiscal 2017 was around 10 percent, while the average increase in the remuneration of the Key Managerial Personnel was in the range of 12-15 percent.

Senior management salaries

The bank's Chief Financial Officer N S Kannan got a remuneration of Rs 5.39 crore, a hike of 62 percent from Rs 3.32 crore a year ago. His basic salary increase was 15 percent at Rs 1.76 crore.

Executive Director Vishakha Mulye’s total salary was at Rs 5.29 crore. She had joined the bank in December 2015 and hence her hike is not comparable.

Former executive director heading the retail portfolio Rajiv Sabharwal, who left ICICI Bank on January 31, 2017, earned a salary of Rs 3.48 crore as against Rs 3.26 crore a year ago. He did not get performance bonus for both the years.

Sabharwal's successor Anup Bagchi, who joined the bank on November 1, 2016, and assumed office as Executive Director from February 1, 2017, was paid Rs 2.02 crore, earning a bonus of Rs 56 lakh.

Former Human Resources head and Executive Director K Ramkumar, who took an early retirement, was paid a total of Rs 3.88 crore, with a bonus of Rs 48.5 lakh.

Banking ordinance, a better plumber for ICICI Bank’s bad loans

The government’s ordinance amending banking regulations—presumably to give the RBI greater powers to fix the NPA problem—will help ICICI’s bad loans

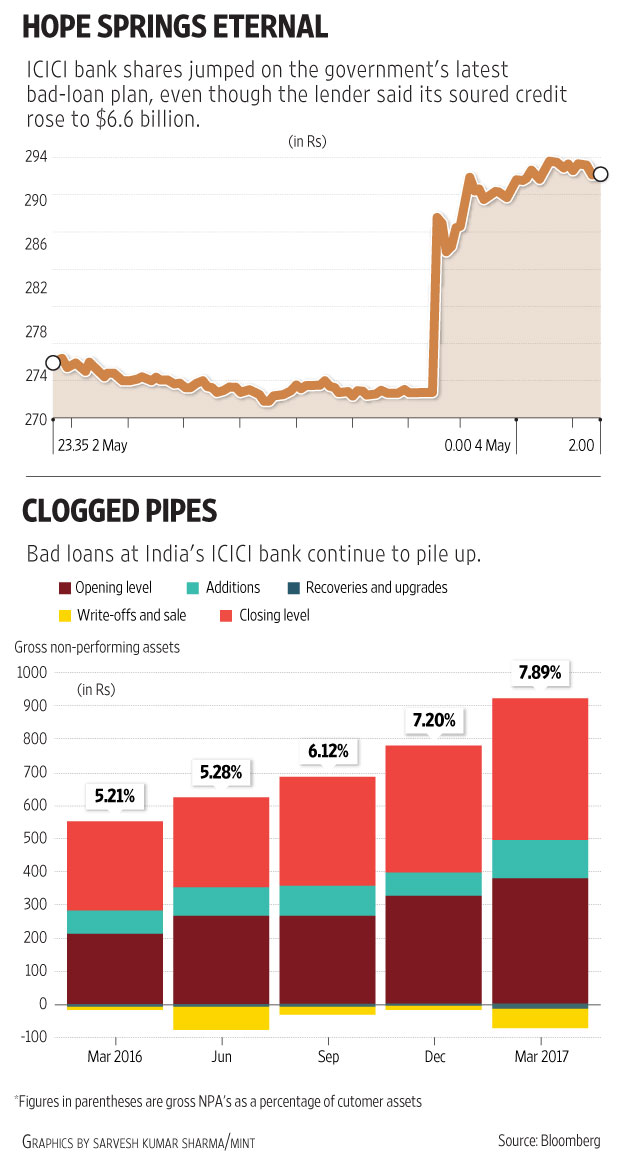

The plumber who’ll sort out India’s bad-loan mess is about to get powerful new tools, and an overflowing toilet will soon be clean. Or that’s how investors are reacting to weaker-than-expected quarterly earnings from the country’s largest private-sector bank by assets.

How sentiment changes. At the end of 2015, when concerns over Indian lenders’ balance sheets reigned supreme, ICICI Bank Ltd had around Rs21,400 crore in gross non-performing assets. The bank announced a 78% jump in NPAs for just the first three months of 2016, and shell-shocked investors pushed the stock down almost 10% in three days.

That was last May. Fast-forward a year, and investors rewarded ICICI Bank’s freshly revealed bad-loan pile of Rs42,500 crore—twice as large as the end-2015 stock—by pushing the shares up as much as 9% Thursday.

The Indian government’s decision late Wednesday to rush through an ordinance amending banking regulations—presumably to give the Reserve Bank of India (RBI) greater powers to fix the $180 billion stressed-asset problem—has made all the difference.

In the absence of details, though, it may be unwise to get too optimistic.

When he launched a special review of lenders’ asset quality in 2015, then RBI governor Raghuram Rajan promised “clean and fully provisioned” bank balance sheets by March 2017. That deadline, like Rajan, has come and gone, and the toilet is getting dirtier. Nothing that Rajan or his successor Urjit Patel have done to stanch the overflow, including letting the banks exchange soured loans for controlling equity stakes, has worked.

What difference will another new wrench make?

To put this in perspective, ICICI’s soured credit is now $500 million greater than the $6.1 billion heap of dud loans at Standard Chartered Plc, which operates worldwide and has almost three times as large a balance sheet as the Indian lender. Worse, the loan-loss cover for ICICI’s $6.6 billion in bad loans is less than $2.7 billion; StanChart’s cushion is almost $700 million thicker.

ICICI and its smaller rivals like Axis Bank Ltd, IndusInd Bank Ltd and Yes Bank Ltd have blamed their lousy March quarter results on one large account. Once Jaiprakash Associates Ltd concludes the sale of its cement assets to billionaire Kumar Mangalam Birla, the builder of India’s sole Formula One track will be able to repay creditors.

Setting that aside, the banks say, the correct gauge is this: With each passing quarter, fewer new loans are turning bad. And let a bad bank take care of the stress that’s already accumulated.

Gadfly has previously argued that a state-sponsored bad bank would be a mistake. As for giving the central bank more powers, the only stick it needs to be able to wield is one that would force lenders to dispose of their soured assets at prices that make sense to asset-reconstruction companies. Those deals are simply not happening.

Last quarter, ICICI managed to offload less than $4 million of bad debt, and another $90 million of special-mention loans. And this at a private-sector lender, which has more latitude for commercial decisions than state-run banks. The latter, which dominate the industry, would be faulted for taxpayer losses if they sold a loan at 30 cents to a private-equity investor who could then get 60 cents out of it.

Besides, with insufficient profits on good loans to offset losses on the sale of bad ones, India’s state-run banks could need more money from taxpayers. That’s a big ask: The government has been stingy on recapitalization, and may be even more so in the last two years of its term as it pumps cash into voter-friendly programs.

It’s up to the central bank now. If those new tools turn out to be inadequate to fix the leak, the overflow of bad assets will start to look like a deluge.

Employees seek to stop Barclays Bank Zimbabwe sale

May 25, 2017

by XOLISANI NCUBE

Barclays Bank Zimbabwe employees have approached the High Court seeking to stop the sale of the financial institution to a Malawian investor or any other buyer, demanding to be given the right of first refusal.

In an urgent chamber application filed by their lawyers, Matsikidze and Mucheche Labour Law Chambers, the 63 workers, led by Sydney Mwalo, pleaded with the court to stop the sale of a stake in Barclays Bank Plc to Malawi-based First Merchant Bank (FMB) until they have shown that they cannot buy the shares.

FMB has been in talks to buy Barclays International’s 68% stake in Barclays Bank Zimbabwe, which has $60 million capitalisation on the Zimbabwe Stock Exchange.

“The respondent (Barclays Bank Zimbabwe) is and, hereby, interdicted from disposing its shares or business to the Malawi investors or any other investors without, firstly, consulting the applicants (workers), as required in terms of the Labour Act,” part of the court papers filed on Tuesday read.

“The respondent (Barclays Bank Zimbabwe) is and, hereby, interdicted from disposing its shares or business to the Malawi investors or any other investors without giving the applicants the right of first refusal or the right of pre-emption and/or complying with the indigenisation and empowerment laws, which mandate that the applicants and other lower level employees to be empowered by forming share-ownership schemes, which allow them to be shareholders before other suitors are considered.”

Barclays Bank plc last year said it was looking to sell-off its African assets and focus on the British and American markets.

According to the affidavit filed by Mwalo, Barclays, in 2016, indicated that it was disposing of part of the shares. The workers claim the matter was concealed from them until they started to enquire but with no success.

Mwalo stated that according to the Labour Act, the issue of change of ownership or disposal of shares was a matter which the law requires the respondents to consult the applicants first.

“In this matter, at all material times the respondents rejected the applicants’ request for a works council meeting in terms of section 25A of the Labour Act to discuss the issue of the sale or disposal of its shares or business to third parties,” part of the affidavit reads.

“The decision to dispose the shares or business to Malawi investors is irrational and will cause customer flight, as most customers are international organisations, who need security of their funds. Thus, the disposal to investors without consulting those customers (will result in) customer and capital flight and subsequently, the bank will collapse and applicants will be jobless.”

The bank was given 10 days to respond to the application or the matter will proceed as unopposed.

Failure of debt-laden telecom operators can trigger defaults, bankers tell government

In a recent presentation to the cabinet secretary, banks said using spectrum as a collateral and extension of spectrum repayment schedule may be needed to salvage this sector.

MUMBAI: India’s top bankers have warned the government that failure in the debt-bruised telecom sector could result in defaults in the industry whose total borrowings amount to a Rs 8 lakh crore. This happens to be more than double the direct exposure banks have made to this sector as disclosed in the Reserve Bank of India’s data.

In a recent presentation to the cabinet secretary that came days before the RBI imposed higher provisioning by banks even on regular telecom loans, banks said using spectrum as a collateral and extension of spectrum repayment schedule may be needed to salvage this sector.

In addition to direct lending by banks to the sector which amounted to Rs 2.63 lakh crore, there is also deferred spectrum payments to the tune of Rs 3.09 crore and third party loans dependent on operators’ contracts of around Rs 1.8 lakh crore, the banks said in their presentation. This would only be further compounded by the expected annual capital expenditure by telecom operators estimated to be Rs 35,000 crore.

Banks estimate that overall annual revenue for the sector will drop by 25% to Rs 1,31,000 crore by March 2019. Banks also argued that with a 20% operating margin, telecom companies would be unable to generate enough funds to service the Rs 5.72 lakh crore debt riddling the sector.

“Certain companies have already started defaulting on payments to banks,” the presentation showed, a copy of which was seen by ET. A query sent by ET to the government remained unanswered. Banks did not comment either.

BANKS’ RECOMMENDATIONS

Banks have recommended some measures that will help telecom companies tackle their debt and have sought tax relief for the sector.

If companies could use spectrum as security, banks could offer more debt and therefore smoothen payouts towards the government-deferred spectrum scheme. At the moment, while companies can offer their licence as a lever to borrow, spectrum, for which bulk of the payments are made, cannot be collateralised under the department of telecommunication rules.

Banks have also urged the government to ease the merger and acquisition norms and hasten permissions to prevent lingering and therefore devaluation of fringe players. A part of this also includes speedy resolution of disputes and permissions.

To help operators who lack ability to raise more funds, banks said a permission to trade their spectrum must be given even if the spectrum was allocated prior to auctions since 2010. For now, companies must pay the price difference between auction price and the allocated price for airwaves, before it can share or trade. Reliance Communications had paid around Rs 5,500 crore before signing a sharing an agreement with Jio.

Banks have urged the government to lower spectrum usage charges, licence fees, and taxes. They have tallied it with telecom taxes prevalent in other Asian countries to demonstrate how Indian companies were paying more.

This can be resolved by restructuring the way adjusted gross revenue was calculated for licence fees, banks proposed. Subscriber statistics show that lucrative customers were concentrating on the top three operators –– Bharti Airtel, Vodafone India, Idea Cellular –– and bargain buyers were focusing on Reliance Jio.

The Reliance Industries company that launched telecom service at an initial investment of Rs 1,50,000 crore in March mopped up most subscribers from tail-ending operators, led by Reliance Communications, as per data released by the Telecom Regulatory Authority of India.“Disruptive and predatory pricing by new operators have resulted in decrease of overall industry revenue over the last quarter along with a drop in government’s revenue share collection,” the presentation showed.

To add to the bankers’ woes, the Reserve Bank of India recently issued a notification to provide for default on some telecom loans even if the accounts were regular at the moment. The government has had its sights set on the over-indebtedness of corporates and has been pushing for measures to write off irrecoverable debt.

INADEQUATE OPERATING PROFIT

Since September, Reliance Jio launched free 4G service for customers to ramp up users. In April, the service became a paid one but at a fraction of the industry pricing. Bankers and telecom officials were moved to action when a recent spectrum payment by a tail-ending operator was missed, and the question of invoking a bank guarantee was raised.

Subsequently, the company paid its dues to the government with interest for the entire month, confirmed an official at the department of telecom. Yet, the question on the validity of some of the bank guarantees was raised as the business case based on which these guarantees were issued has changed.

The World's Largest Banks in 2017: The American Bull Market Strengthens

MAY 24, 2017

Chinese banks remain the largest corporations on earth, but a resurgent Wall Street means competition is increasing in the global banking industry.

Industrial and Commercial Bank of China and China Construction Bank remain the two biggest corporations in the world, according to the 2017 Forbes Global 2000, but U.S.-based competitors are gaining major ground. JPMorgan Chase has eclipsed Agricultural Bank of China as the world’s third largest bank and it is Wells Fargo that now rounds out the top four in banking. In fact, all of America’s big six banks gained ground in the industry.

Bank of America and Citigroup are both firmly among the global top-10 in banking. In 2016, Goldman Sachs and Morgan Stanley were among the industry’s fastest risers, supplanting Asian and European banking giants including Industrial Bank and UBS . Driving the American banking bull is resilient top line growth, led by a strengthening U.S. dollar, stable gross domestic product growth and the Federal Reserve’s increase of short-term interest rates. And it won’t slow anytime soon, U.S. banks have been among the best performers on global markets since the fall, as President Donald Trump vows to roll back regulations and increase lending.

Profits at America’s big six banks are expected by analysts to hit post-crisis highs in 2017 as a combination of rising rates and business friendly policy drive their bottom lines. Trouble spots in the U.S. economy, whether it is rising auto and student loan defaults, are not expected to outweigh positive fundamentals such as rising wages, falling unemployment and near-record low mortgage and credit card default rates.

Chinese banks, which dominated last year’s Forbes Global 2000, face a murkier outlook. Global investors continue to worry about credit losses inside the Chinese banking system. A growth scare in early 2016 caused wild market swings around the world as the country’s economic growth fell below 7% on an annualized basis. This slowing economy means profits at China’s biggest ten banks fell in 2016, allowing U.S. lenders to pick up market share.

In 2017, investors will be closely watching pressures inside the Chinese banking system, from rising leverage to weakening asset quality and even write-downs. Politics may prove to be tricky as well. The Trump administration’s focus on renegotiating trade deals and its close watch of exchange rates between the U.S. dollar and the Chinese yuan could lead to added volatility. Amid this backdrop, the banking ‘big four’ is now balanced between U.S. and Chinese lenders.

In Europe, banks continue to wrestle with the scars of the 2008 crisis and troubled times for the currency union. French lender BNP Paribas is the only EU-based bank to make the global top-10. Powerhouse lenders in the region such as HSBC, UBS, Intesa Sanpaolo and Credit Agricole were some of the industry’s biggest fallers. With Great Britain negotiating an exit from the European Union and firms from Barclays to Deutsche Bank and Credit Suisse still raising capital, global investors are yet to rush back into regional lenders.

Brazil, having recently exited one of the worst recessions in the country’s history, is beginning to attract investor attention and lenders such as Itau Unibanco and Banco Bradesco are back on the rise. Plagued by plunging oil prices in 2016, Russia is also on the rise. No bank in the top-25 gained more than Moscow-based Sberbank .

Among the world’s 25 largest banks, China houses the most with eight firms, while the U.S. places second with seven spots. Canada and Brazil each had two spots while Spain, France, Japan, Russia, the Netherlands and the United Kingdom had a spot apiece.

Germany and Italy, the industrial engine of the Eurozone, did not have a bank ranked in the top 25 globally, nor did Switzerland. Volatile emerging markets like China, Brazil and India continue to drive global growth expectations over the long-run, but right now it is the U.S. banking industry which is resurgent, proving the stability of U.S. lenders remains formidable competition.

Move & Mobilise from now on

AIBEA – AIBOA’s

MASSIVE MORCHA TO PARLIAMENT

On 15th SEPTEMBER, 2017

Stop Banking Reforms

Save Banks from Defaulters

Strengthen Public Sector Banks

VIBRANT BANKING – VIBRANT INDIA

AIBEA THIS DAY – 29 MAY

|

1986

|

AIBEA General Council meets at Calcutta.

|

1989

|

Allahabad Bank employees observe one day strike in U.P.

|

|