Private NPAs

Even new generation private sector banks are showing asset quality deterioration in stressed sectors

Anand Adhikari

In April last year, Axis Bank came out with a 'watch list' of Rs 22,000 crore-plus stressed corporate loans, accounting for 15 per cent advances to companies. The bank, headed by Shikha Sharma, a former ICICI banker, admitted that 60 per cent of these loans would become non-performing assets, or NPAs, in the next two years. To the bank's surprise, half turned into full-blown NPAs by the end of the first year itself, that is, by March 2017. The bank is now staring at further slippages as a bulk (almost 60 per cent) of the remaining loans in the list have been given to the battered power sector. Exposure to other troubled sectors such as steel, oil & gas and cement could create further problems.

Things have turned so bad at the new-generation private sector bank that it now has one of the highest gross NPAs among private sector banks (5.04 per cent). The bank's gross NPAs, at Rs 21,280 crore, are half its revenues for the year. It is not alone. Other private banks, such as ICICI Bank, have also seen a spurt in NPAs in the last few years. The culprit, in most cases, is these banks' lending to core sectors, which have been in deep depression for the past few years. "Anybody (public or private sector bank) who has lent to the infrastructure sector has suffered," says Abizer Diwanji, National Head (Financial Services), EY India.

What is worrying private banks now is the Reserve Bank of India's, or RBI's, move to ensure higher provisioning for even standard assets, or good companies, if they are in stressed sectors. "This will have a direct impact on banks' profitability as they will have to make higher provisioning (from 0.40 per cent to 4 per cent) for even well-paying assets," says a consultant. Diwanji, however, says that the RBI is trying to make banks more resilient. "There is enough (stress) in the system that needs to come out," he says.

The trend of rising NPAs in private sector banks is surprising, as this was conventionally considered an intractable problem only for public sector banks or PSBs - which were solely blamed for having a disproportionate share of total banking sector NPAs. Though, for most PSBs, the gross NPA figure is still more than 8-10 per cent, much higher than that for their private sector counterparts.

Experts say it is not right to say that private sector banks have been lax in lending. They add that it is the global environment that has turned topsy turvy due to excess capacity and over-leveraging. Apart from this, there has been a slowdown in the domestic economy. All this is creating stress on corporate balance sheets and affecting companies' ability to pay banks. "Jaipraksh was a standard asset till a few months ago. The deal (with UltraTech) will be completed soon and the provisioning will be written back in profits," says a private sector banker whose bank had to make NPA provisioning for the company because of the non-completion of the deal.

The bad asset resolution mechanism is also not working as expected. In many cases, the call has to be taken by public sector bank consortium members, and decisions such as haircut and one-time settlement get stuck for months.

For private sector banks, another and more immediate worry is exposure to the telecom sector. The RBI has asked banks to make higher provisioning than the regulatory minimum for standard assets in stressed sectors by June this year. Some private banks have telecom exposure , which is a standard asset. So, even when the asset is good, the banks will be forced to ensure higher provisioning for it, though some private sector banks are already proactive in dealing with loans to such sectors. IDFC Bank, for example, has been ensuring higher provisioning for telecom much before the RBI circular. In 2015/16, ICICI Bank built a contingency fund of `3,600 crore for slippages in sectors such as steel, mining, power and cement. The bank had to utilise the fund in 2016/17.

While private sector banks are proactive, they are also better capitalised than the PSBs and so in a better position to absorb provisioning shocks. RBI Deputy Governor Viral Acharya recently summed it up well when he said that the doubling of stressed assets is a cause of worry for private sector banks, but their ratio of stressed assets to gross advances is far lower and capitalisation levels far higher.

The private sector banks also have a more diversified book than the PSBs. Their retail advances are showing robust growth that can compensate for lower credit offtake in the corporate sector. Axis Bank's corporate book, for example, was stagnant in 2016/17, while retail advances grew 21 per cent. Unlike PSBs, which face constraints while raising capital, private sector banks have been raising huge amounts of capital.

Many say the current experience will stand private banks in good stead as exposure to corporate loans increases in future.

In FY17, banks went easier on defaulters

RADHIKA MERWIN BL RESEARCH BUREAU May 28, 2017

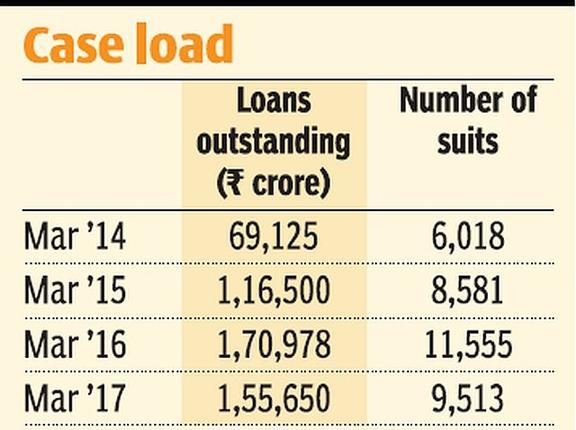

Bad-loan suits drop after rising sharply in the preceding 2 years

While the RBI has been pushing for an action plan to implement the NPA (non-performing asset) ordinance, banks have been somewhat lax in taking legal recourse to recover bad loans.

According to data published by Credit Information Bureau of (India), of the 9,500-odd cases filed by banks and financial institutions, in the case of loans above ₹1 crore, defaulters owed banks about ₹1.5 lakh crore as of March 2017, which is 9 per cent lower than the amount in the previous year.

As of March 2016, banks had filed around 11,500 cases on ₹1.7 lakh crore worth of outstanding loans. The decline follows the sharp increase in suits filed in the preceding two years.

Banks that normally file a suit as a last resort for recovery took this route more often between 2014 and 2016. As of March 2015, bad-loan suits had shot up 68 per cent (in value) over the previous year, followed by a further 47 per cent in March 2016. Banks and financial institutions submit the list of suit-filed accounts of ₹1 crore and above, and quarterly updates to CIBIL as well as the RBI. According to a few bankers, there are three key reasons for the drop in suits filed: one, banks have been increasingly selling their bad loans to asset reconstruction companies (ARCs). As such sales immediately take the bad loan off the banks’ books, these cases may not appear in CIBIL records. In 2016-17 banks sold bad loans worth ₹40,000 crore to ARCs, against ₹20,000 crore sold in 2015-16.

A few bankers also believe that in some cases filed in the past, banks might have reached a one-time settlement with borrowers.

Also, with the RBI rolling out new tools for restructuring loans and dealing with NPAs — Strategic Debt Restructuring and Scheme for Sustainable Structuring of Stressed Assets — it is likely that banks did not file as many fresh cases as in the past. “Banks have been awaiting clarification on various guidelines from the RBI regarding NPAs over the past year. Also, expectations ran high on some relief from the Centre and the RBI on the bad loans front. This could have kept banks from taking legal recourse to recover bad loans,” says Nirmal Gangwal, Managing Director, Brescon Corporate Advisors, a corporate debt restructuring advisory firm.

Also, he believes that given the uncertainty in the banking system, decision-making has slowed.

“Weak finances of banks could be another reason. Filing cases to recover bad loans would require banks to make higher provisioning, depending on the assessment of the underlying collateral,” adds Gangwal.

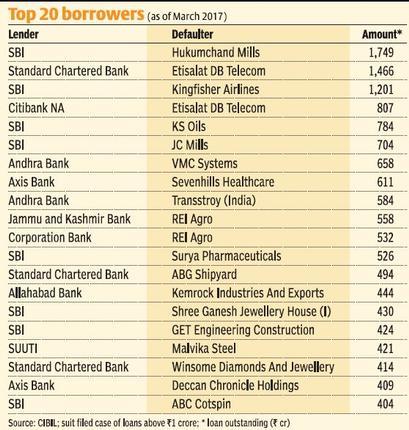

Top borrowers

As of March 2017, the top 20 borrowers owed banks about ₹13,600 crore.

Hukumchand Mills tops the list, owing around ₹1,700 crore to largest lender SBI. This is followed by Etisalat DB Telecom, Kingfisher Airlines, KS Oils, JC Mills and VMC Systems, among others.

Many of the defaulters in the CIBIL list have been featuring time and again over the last two to three years. Kingfisher Airlines, Etisalat DB Telecom and Deccan Chronicle are a few names that have been in the list since March 2014. In many cases, borrowers have defaulted across lenders. SBI, Kotak Mahindra Bank and IFCI are lenders that have filed cases against Hukumchand Mills, for total dues of about ₹1,750 crore.

Etisalat DB Telecom (₹2,273 crore), Kingfisher Airlines (₹1,633 crore), Deccan Chronicle Holdings (₹760 crore), and REI Agro (₹2,725 crore) are among other big-ticket listed names against whom multiple lenders have filed suits.

LIC too

Aside from banks, a few financial institutions have also filed cases. The Specified Undertaking of Unit Trust of India (SUUTI), for instance, has filed 90-odd cases against defaulters, who owed it about ₹1,280 crore as of March 2017.

As of December 2016, LIC, too, had filed 30-odd cases against defaulters, who owed the insurer about ₹3,340 crore. Deccan Chronicle, Hamco Mining and Smelting, Punjab Wireless, Tulip Telecom and REI Agro were some of its top defaulters.

FinMin starts process to find new SBI chief

PTI NEW DELHI, MAY 28: BUSINESSLINE

Arundhati Bhattacharya’s term ends on October 6

The finance ministry has initiated the process for finding new chief of the country’s largest lender State Bank of India (SBI) as Arundhati Bhattacharya’s extended term comes to an end on October 6.

“Department of Financial Services has communicated to Banks Board Bureau the emerging vacancies at the top level of PSU banks which will have to be filled during course of the year,” a senior finance ministry official said.

This also includes chairman and one managing director of the SBI, which alone has market share of more than 20 per cent.

Bhattacharya will complete her four—year term as chairperson of SBI on October 6.

Besides chairman, SBI has four managing directors looking after different departments.

The post assumes significance as the bank has recently merged five associates and the Bharatiya Mahila Bank (BMB) pushing SBI into the league of top 50 banks globally in terms of assets.

State Bank of Bikaner and Jaipur (SBBJ), State Bank of Hyderabad (SBH), State Bank of Mysore (SBM), State Bank of Patiala (SBP) and State Bank of Travancore (SBT), besides BMB, merged with SBI with effect from April 1. The process of integration would at least take a year.

The government had in February approved the merger of these five associate banks with SBI. Later in March, the Cabinet approved merger of BMB as well.

SBI first merged State Bank of Saurashtra with itself in 2008. Two years later, State Bank of Indore was merged with it.

For the fourth quarter ended March 2017, the bank reported more than doubling of its net profit on the back of increased lending and reduction in provisioning for bad loans.

Net profit of the bank on standalone basis rose to Rs. 2,814.82 crore for the March quarter as against Rs. 1,263.81 crore in the same period of previous fiscal 2015—16.

For the entire fiscal ended March 2017, the net profit of the bank improved by 5.36 per cent to Rs. 10,484 crore as against Rs. 9,951 crore in the previous fiscal.

With stock prices inching up, SBI has lined up share sale through which it intends to raise Rs. 15,000 crore during the current fiscal.

It is in the process of appointing six merchant bankers for managing its proposed share sale. The central government holds 62.22 per cent stake in the bank as of March 2017.

Banks Recovered Only Rs. 47kcr of Loans in FY17

Gross NPAs of 37 listed banks were at 7.1 lakh crore at March-end, 2017

Mumbai: Banks with ambitious targets for loan recoveries last fiscal have floundered. An ET analysis of the top 10 state-run and private banks has revealed that these banks managed to recover only Rs. 47,240 crore in the financial year gone by out of which Rs. 16,000 crore came in Q4 alone.

Gross non-performing assets of 37 listed banks were at Rs. 7.1 lakh crore at the end of March 2017 against Rs. 5.71 lakhcrorethesametimein2016.Lack of capital at the asset reconstruction companies and the fear of witchhunts by investigative agencies put a freeze on loan recovery.

“The underlying asset to which banks have lent is not performing, so recovery and upgradation will take some more time,” said. Siddharth Purohit, senior research analyst, Angel Broking. “Bigger recovery numbers will be difficult to achieve in FY18 as well, though some recovery may happen on a case-to-case basis.”

Among the PSU sector pack, only Punjab National Bank and Canara Bank managed to deliver on their thrust on bad loans and recovered Rs. 10,677 crore and Rs. 10,017 crore for the full year FY17, respectively.

The country’s largest lender, State Bank of India, recovered Rs. 5,197 crore inFY17.ForthequarterendedMarch 2017 its recovery from bad assets stood at Rs. 1,203 crore, which was a little higher than the December 2017 figure of Rs. 1,003 crore. The bank had recovered Rs. 1,627 crore in the quarter ended March 2016. Bank of Baroda, the third largest state-run lender, recovered Rs. 4,088 crore, Bank of India Rs. 4,598 crore, Central Bank of India Rs. 2,378 crore and Union Bank Rs. 1,388 crore in the financial year 2017.

“Post the recent government and RBI action, expectations of progress on stress asset resolutions have gone up,” said Ashish Gupta, analyst, Credit Suisse. “However, given the low 30% provision cover on these loans, progress will necessitate additional provisioning and capital. Provisions needed on recognised stressed assets are equivalent to 3-9 years of operating profits.” Among the private banks, Axis Bank performedmuchbetterthanICICIBank.

While for the full year Axis Bank’s recoveries and upgradation stood at Rs. 4,367 crore, ICICI did Rs. 2,538 crore.

Hope to see consolidation among government-owned banks in 2-3 years

If there are fewer players with deep pockets, they dominate and the sector does well

Larger banks have better market access and should be able to merge with smaller banks

Moelis & Company, which started its India operations in 2012, works with a team of 14 bankers headed by veteran investment bankerManisha Girotra. Prior to Moelis, Ms. Girotra was the chief executive of Swiss bank UBS’s India operations. Moelis, which advised several high profile deals like the sale of Japyee’s cement assets to Aditya Birla Group, is upbeat on the opportunities to resolve stressed assets in India and wants to play an active role in the sector.

The Centre has recently amended the Banking Regulation Act that gives more power to the RBI in resolving stressed assets. Does this present an opportunity for you?

I believe the part of the NPA problem will be resolved with economic growth reviving. Growth should be robust in the next two-three years which will resolve the NPA problem. Having said that some of them will need restructuring, some of them may need a change in ownership. There is a political will to see our banks healthy again.

There is a strong opportunity for Moelis in the restructuring space. We had participated in some of the deals like selling of Jaypee’s cement asset to Aditya Birla. We were also involved in the restructuring of Essar’s coal assets in the U.S., to name a few. I see more such opportunities for us. Restructuring is a large part of Moelis’s global business. I think the opportunity exists here too because of the stressed situation in banks.

It is heartening to see that there is a political will. The whole joint lender’s forum could not come to a consensus because there were multiple players — what was really needed was someone to drive it. So I am very positive on what has happened. With the Act amended, we are hopeful to see all of this debt recast implemented properly and we expect in the next 12-18 months a lot of these problems unwinding.

Many private equity funds were awaiting regulator’s clarity for participating in the stressed assets sector. Will the change in Act help?

The conversations are all alive with the banks. The new ordinance will help. You will see a lot of private equity funds coming into India to acquire stressed companies in the next 12-18 months.

RBI has recently revised the norms for prompt corrective action (PCA) and imposed restrictions on some banks. Do you see this as a prelude to consolidation among public sector banks?

I don’t know, but I hope they are. I think in the state-owned bank’s space there is a lot of scope for consolidation.

The larger banks which are better capitalised, have better market access and should be able to merge with the smaller banks. There should be fewer banks but stronger banks. Whichever sector it is, if there are fewer players with deep pockets, they dominate and the sector does very well. We have seen it in the telecom sector. I really hope to see consolidation among public sector banks in the next 2-3 years as the sector needs to consolidate.

But bigger banks are also facing asset quality headwinds…

The financial sector is getting a lot of flows from the public market. At the moment, state-owned banks aren’t getting the share of these capital flows. As it is able to walk through some of the NPA problems, we will see funds flowing into these banks again.

So then they can raise funds through FPO, QIP etc., and get capitalised. So it is a bit of a two-pronged strategy… as you see some of the NPA problems get resolved, the market will have confidence on them, and then they can get capital and then drive growth and consolidation.

The merger of public sector banks is a political hot potato. Do you think the government will push consolidation?

The government is really serious about the business, they are serious about solving the NPA problem. We have seen the political will they have demonstrated in the last 18 months…it is unprecedented…I have not seen anything like this in my career. So they want to strengthen their banks. So, I hope the next step will be consolidation among state-owned banks.

How do you see mergers and acquisition activity panning out in the banking and financial sector?

The sector will remain active, there is a lot of capital coming into the sector. Rather than bank-to-bank, there is a lot of consolidation activity in bank to NBFC, bank to MFI which provide you certain geography, certain product … and I think you will see more of those happening. Also, a lot of capital is chasing the fintech players. The whole demonetisation exercise and drive to digitisation gave these companies a huge push. That space also realises that there is merit in scale. So, you will see consolidation for the reason of scale. I think the fintech sector will remain active in the 12-18 months with regard to consolidation.

Last year we have seen healthy M&A deals. How do you see the demonetisation exercise impacting such deals?

Demonetisation has no consequence on M&A activity. Last year we had $60 billion of M&A. A refreshing trend that I have seen is that a lot of domestic M&As are happening… earlier you have not seen Indian entrepreneur selling to an Indian entrepreneur or an Indian entrepreneur paying a higher multiple for an Indian company. There is always this build versus buy argument.

But today, they are willing to pay the multiple. In my career, M&As were always inbound or outbound. This is the first time I am seeing domestic M&A outnumbering inbound plus outbound. Out of the $60 billion of M&A last year, $30 billion would be domestic, $20 billion was inbound and $10 billion would be outbound.

Do you see this trend continuing?

Domestic consolidation will remain an important theme because people are realising India is too big a country and to play in this country you need to have a scale. The scale provides you cost reduction opportunities, market access etc. Also, there are some companies where the second generation does not want to involve in business. So they are happy to monetise, earlier this never used to happen! The other trend we are seeing is that the private equity players have actually been able to monetise stake. They are not only exiting through IPOs but they have been able to sell companies. That is a very important trend because they are able to demonstrate that if they are able to put capital in India, they are also able to exit capital out of India

Rs. 3,045 cr. in rural scheme wages yet to

Kerala, Uttarakhand worst hit as pay orders are pending

Delays in the payment of Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) wages have mounted drastically in April-May 2017, as Fund Transfer Orders (FTOs) worth Rs. 3,045 crore are yet to be processed by the central government’s National Electronic Fund Management System (NEFMS).

According to data collated from the MGNREGA website by the MGNREGA Sangharsh Morcha, a platform that tracks the implementation of the workfare programme, 63% of the unprocessed FTOs were generated in April-May. The processing delay was highest in the cases of Kerala and Uttarakhand, where no FTOs have been processed since April 15. This follows another period of 20 days in March-April 2017 when no FTOs were processed by the Centre.

Eligible for compensation

As per Schedule II of the Act, an MGNREGA worker must be paid within 15 days of completing his allocated tasks. A delay in payment, for which the worker must be compensated, has to be calculated from the 16th day after task completion, till the time the money is credited in the worker’s account.

A note released by the MGNREGA Sangharsh Manch pointed out that the MGNREGA Management Information System (MIS) has been programmed to calculate the compensation in a flawed manner.

Systemic failure

It calculates the delay only till the second signature on the FTO from the state government, after which the pay order goes to the central government for processing.

“According to a recent study, it takes, on an average, up to 25 days for the payment to reach the worker even after the FTO has been signed,” said Ankita Aggarwal of the MGNREGA Sangharsh Manch. “But this delay and unexplained delays such as the one caused by the current non-processing of the FTOs, is not accounted for in the system.”

The Ministry of Rural Development has so far not provided any explanation for the irregularities in the FTO processing nor the flawed calculation of the payment delays.

The FTOs haven’t been processed since May 2 in the case of Karnataka, since May 8 for Bihar, Jharkhand and Rajasthan, and May 5 for Himachal Pradesh.

This has resulted in workers in these States not having been paid more than 15 days after completion of work. However, the MGNREGA MIS (management information system) does not capture this delay denying them compensation.

“The government must adopt a system for MGNREGA payments that is reliable and not vulnerable to gross irregularities such as repeated delays in the processing of FTOs,” Ms. Aggarwal said.

No comments:

Post a Comment